Foresight Analysis no. 284, 2 March 2023.

This analysis was finalized on 22 February 2023. It has been translated from French by Chris Turner.

Vladimir Putin’s speech on 21 February 2023 marked the first anniversary of Russia’s war against Ukraine. Along the same lines as his Red Square speech of 30 September 2022,[1] it emphasizes the international dimension the Russian president ascribes to the conflict, which situates it in a decades-long series of clashes with the North Atlantic Treaty Organization (NATO). For their part, the Western allies are wholly opposed to the idea of reducing their support for Ukraine, which ‘must not be allowed to lose’.

The counter-attacks launched by Ukraine in the Donbas in late summer 2022 were already a turning-point in the conflict with Russia, representing a major new setback for the Russian army. The enhanced military mobilization of the population announced in late September 2022 by Vladimir Putin and the annexation of four Eastern Ukrainian regions concluded that sequence and opened another, particularly uncertain and dangerous phase. Neither Russia nor the Ukrainian bloc have defined precisely what might constitute defeat or acceptable victory for them, apart from maximalist aims of the conquest or total preservation of Ukrainian territorial sovereignty. The frontlines have stabilized for the moment on account of the winter and the balance of forces. Spring could, however, play a part in a new escalation on the ground. The extent of that remains difficult to determine, while the threat of nuclear weapons continues to hover over the conflict.[2]

In this unstable context, what course is this war likely to take in the years to 2025? This question requires us to study a number of key variables, which are equally as uncertain: the capacity of the Russian army to rebalance the situation on the ground by mobilizing its population; the conditions for Vladimir Putin retaining power; the persistence of Western support in the face of the danger of escalation, of strains on military stockpiles or a deterioration in the socio-economic context. How the position of China might develop and potential reversals in the attitudes of non-aligned countries like Turkey, India and Israel are also major variables.

This document is a continuation of the work carried out by Futuribles from the beginning of the war (cf. ‘Round Table’ of 11 March 2022[3]). It aims to update the key messages established in July 2022, which study the most crucial variables in detail, and the scenarios for the development of the conflict that ensue from these and were published last summer.[4]

It aims, in this way, to offer a precise interpretative grid for the conflict, by defining it but also by examining the preconditions for a lasting peace through study of the stances of the various parties concerned and by tracking the more general geopolitical and geo-economic consequences of the conflict (key messages, part 1). Given the many uncertainties, the time period for this deliberative foresight exercise is kept short (two years), but the scenarios proposed aim to cover the full field of possibilities (part 2), in order to equip the actors concerned, both public and private, with adequate decision-making tools.

Reminder of the Methodology

To construct the analyses presented here, an iterative work process was adopted:

• Gathering lines of questioning from the members of Futuribles and their contributions to orient our thinking and to prioritize themes (working session of 21 April 2022).

• Consolidation and development of six scenarios by analysing some major variables (the military balance of forces on the ground, the play of alliances etc.) and thanks to interviews carried out with a number of experts.

• Analysis of the direct implications of the three scenarios differing least radically in military terms from the present course of events for global economic, agricultural and energy flows, for humanitarian crises, for the play of alliances and for the role of international governance (Foresight Analysis published in July 20221).

• Summer-Winter 2022: continuous monitoring and updating of the scenarios and the key messages.

• January 2023: updating session with the members of Futuribles International and a number of experts.

• March 2023: publication of key messages and updated scenarios.

We warmly thank Sébastien Abis, Matthieu Anquez, Didier Billion, Gilbert Cette, Elvire Fabry, Thierry Hommel, Nicolas Mazzuchi, Diane Mordacq, Pierre Papon, Christian de Perthuis, Thierry Pouch, Philipppe de Suremain and Nicolas Werth for their valuable contributions.

N.B.: Futuribles International bears sole responsibility for the content of this document.

1. Ségur Marie (ed.), ‘What Scenarios for the War in Ukraine: The Progression of the Conflict and Geopolitical Trajectories to 2025’, Foresight Analysis no. 272, 12 July 2022, Futuribles International. URL: https://www.futuribles.com/what-scenarios-for-the-war-in-ukraine-the-progress/. Accessed 21 February 2023.

Contents

Part 1. Key Messages

War and Peace: Defining the Conflict, Identifying the Outcomes

1. Regional and Proxy War. The Post-Cold-War International Order Disrupted

2. Maximalist War Aims and Military Stalemate: No Prospects of a Lasting Peace

Who are the Protagonists?

4. Ukraine on Western Life-support. How Sustainable is the War Effort to 2025?

6. Turkey, a Regional Power Central to the International Issues of the next few Years

7. China and Russia: Interests strongly Converging, but as yet no Overt Military Alliance

What are the Broader Geo-economic and Geopolitical Consequences?

9. Emergence of a China-US Decoupling over Strategic Sectors

11. Fears of a Major Global Food Crisis not yet Realized, but Risks Remain

12. Economic and Political Dissensions within the EU: the Future of European Equilibrium Unresolved

Part 2. Updating of the Scenarios

Scenario 1. Stalemate and Instabilities

Scenario 2. High Intensity Conflict in Ukraine. Towards a World of Blocs

Scenario 3. Fears, National Self-Interest and Territorial Expansion of the Conflict

Scenario 4. Russian Territorial Objectives Achieved

Scenario 5. The Territorial Integrity of Ukraine preserved

Scenario 6. Global Conflict and Russia Doubling Down

Concluding Summary: Potential Change in the Balance of Forces and Flipping between Scenarios

Part 1. Key Messages

War and Peace: Defining the Conflict, Identifying the Outcomes

Regional and Proxy War, the Post-Cold-War International Order Disrupted

In strictly military terms, this war is a regional conflict, geographically confined within the borders of Ukraine. However, the area of confrontation is, in reality, much wider, as is attested by the panoply of economic, trade and financial sanctions to which Russia has been subjected (amounting to what has been called a ‘weaponization of everything’[5]). In the coming months, that area could extend further with new sanctions, a possible increase in attacks on strategic international infrastructures, and the intensification of disinformation and internal destabilization operations. It is in this regard that the war, though regional and perceived as such by countries outside Europe, greatly affects states and populations geographically far distant from it.

Moreover, for Vladimir Putin, the war is a continuation of several decades of more or less implicit clashes with NATO and, more broadly, with the West (cf. his Munich Speech of 2007). At the same time, the Western allies refuse to involve themselves directly in the conflict, in order to avoid nuclear escalation, but are giving Ukraine massive support: military equipment, information and training, financial and humanitarian aid and, further to this, are imposing sanctions aimed at weakening Russia’s capacity to maintain its war machine. In this sense, NATO may be seen as conducting a proxy war with Russia.[6]

The war is not just territorial or economic. It also has a major political and cultural significance. It is this aspect that gives it a resonance among other authoritarian regimes (China, Iran etc.)—and also among countries of the global South who are set on revenge for Western colonialism and a reversal of the historical balance of forces of neo-liberal globalization. This geopolitical reordering is at the heart of the Russian strategy. Russia is out to destabilize the Western powers through information warfare and a policy of increasing influence in the countries of the South. This is particularly the case in Africa. The growth of Russia’s trade with India and China is also part of a broader ambition to eventually challenge the centrality of the US dollar in international commerce.

As part of this opposition, the democratic norms and values traditionally embodied in American and European institutions are increasingly contested. Multilateral organizations seem to be outflanked, if not indeed obsolete. The vetoes exercised by Russia and China paralyse the UN Security Council, being more a part of an international disorder than the emergence of an alternative order that is as yet hazy in its details. Moreover, the increasing panoply of trade sanctions and protectionist politics points up the inability of the World Trade Organization (WTO) to maintain the principles of free trade.

Map 1. Distribution of votes in the UN General Assembly on the resolution condemning the Russian invasion of Ukraine, 2 March 2022

The abstention of 35 countries out of 193 on the UN resolution of 2 March 2022 condemning Russian aggression and demanding the withdrawal of its troops from Ukraine clearly showed the resolve of certain countries of the global South not to align with the Western position in this conflict.

Source: “10 points synthétiques sur le vote à l’Assemblée générale des Nations unies”, Le Grand Continent, 3 March 2022. URL: https://legrandcontinent.eu/fr/2022/03/03/10-points-synthetiques-sur-le-vote-a-lassemblee-generale-des-nations-unies/. Accessed 21 February 2023.

Maximalist War Aims and Military Stalemate: No Prospects of a Lasting Peace

Russia actually scaled back its initial war aims following the failure to capture Kyiv quickly and redirected its war effort into the Donbas region and along the Black Sea coast. But the annexation of the four oblasts of that region underscores how it has maintained ambitious political and military objectives. There is good cause for this, the political future of Vladimir Putin being linked to the outcome of the war. It seems difficult, then, for the Russian leader to accept a defeat.

On the Ukrainian side, President Zelenskiy has maintained the aim of restoring Ukraine’s pre-2014 borders. Having in early October adopted a decree against negotiations with Vladimir Putin,[7] he calls in a ten-point peace plan for the full payment of reparations by Russia and for its leaders to be arraigned before a war tribunal.[8] This position is supported by the allies who favour a hard line against Moscow (Baltic States, Poland, UK). Whereas President Macron of France sought initially not to leave the role of mediator solely in the hands of Turkey[9], France and even Germany now increasingly seem to back unconditional support for Ukraine. This consolidation of the European alliance can be explained, among other things, by a realization of the inflexibility of Russian war aims and the perception of these as a threat to the European Union (EU) and its values, but probably also by more pragmatic logics. Maintaining an intransigent stance towards Russia might be regarded by the European states as a means of not ‘losing face’ on the international stage at a point where massive support for Ukraine is becoming the most consensual position. However, the already colossal costs of the war and their accumulation without any prospect of significant recovery of territory might eventually induce the Ukrainian president to compromise on his ambitions of fully returning the country to its previous borders.

The maintenance of the war effort and Ukraine’s capacity to contain the Russian forces—and even to conduct new counteroffensives—are dependent on the continuance of Western support, which could set a red line on the re-conquest of Crimea in order to limit the risks of non-conventional escalation. The gradual character of the increase in NATO military support has, up until now, been key to retaining control of that escalation and holding on to potential additional levers of pressure. While Washington was for a long time reticent about sending HIMARS rocket-launchers (High Mobility Artillery Rocket Systems) which have made it possible to strike deep into the Russian lines, the delivery of military hardware as symbolic as tanks has now been agreed to, and sending fighter aircraft is no longer taboo for some allies. The so-called ‘sunk costs fallacy’[10] is also leading NATO to speed up its support at a crucial moment when Ukraine seems vulnerable in the face of augmenting Russian military force. For the USA, a lasting weakening of Russian military potential would enable European security to be maintained in the medium term while their strategic concerns shift towards China. In January 2023 a report by the Rand Corporation think tank, which is influential in the field of national security, stressed the risks to US interests that might ensue from a stalemate.[11] Earlier in the conflict President Biden was able to declare that Vladimir Putin ‘cannot remain in power’.[12] Nevertheless, last autumn the American general Mark Milley declared that he did not believe either of the belligerents could achieve total military victory, thereby creating pressure for negotiations.[13] The continued existence of some multilateral initiatives, such as the agreement on grain exports through the Black Sea or the inspections of nuclear installations by the International Atomic Agency (IAA), underscores the fact that we have not yet reached the point of no return in terms of escalation.

A halt to fighting in the short term, by way of a ceasefire, for example, will not necessarily spell long-term peace. On the contrary, Russia could take advantage of this to reorganize its military forces and relaunch a more ambitious offensive at some point in the coming decade. The next objective of the Russian president may conceivably be the total conquest of Ukraine—and even Transnistria—with an eye to restoring so-called Novorossia. A Korean-type scenario can also not be ruled out, in which there is no peace treaty, but an armistice that finds expression in a demilitarized zone between the two countries. Given the dangers involved, it seems urgent to begin negotiations to end the war, but there will be serious issues in such negotiations, relating to justice for the war crimes committed by the Russian regime, the credibility of Russia’s commitments with regard to international law, and Europe’s security architecture. Looking forward to 2025, the conditions required for lasting peace seem difficult, then, to achieve and there is a genuine risk of escalation.

How to Gauge Levels of Attrition in this Conflict?

With this conflict, high-intensity war has returned to Europe, two states clashing in quite classical ways. Among other things, artillery is playing a major role in a war of position structured around relatively stable fronts, which is reminiscent, in some respects, of the First World War. Within this framework, the attrition of the two warring parties represents a major variable in the way the balance of forces is developing. Matthieu Anquez, the founding Chair of ARES Stratégie and a scientific adviser at Futuribles International, describes the dynamics of attrition playing out in a conflict as a triptych structured around human and material losses and the morale of the belligerents, war being, as Clausewitz argued, a clash of wills. The dynamics of attrition should not be taken as the single key to analysing the war in Ukraine, but it contributes greatly to understanding how the military balance of forces is evolving.

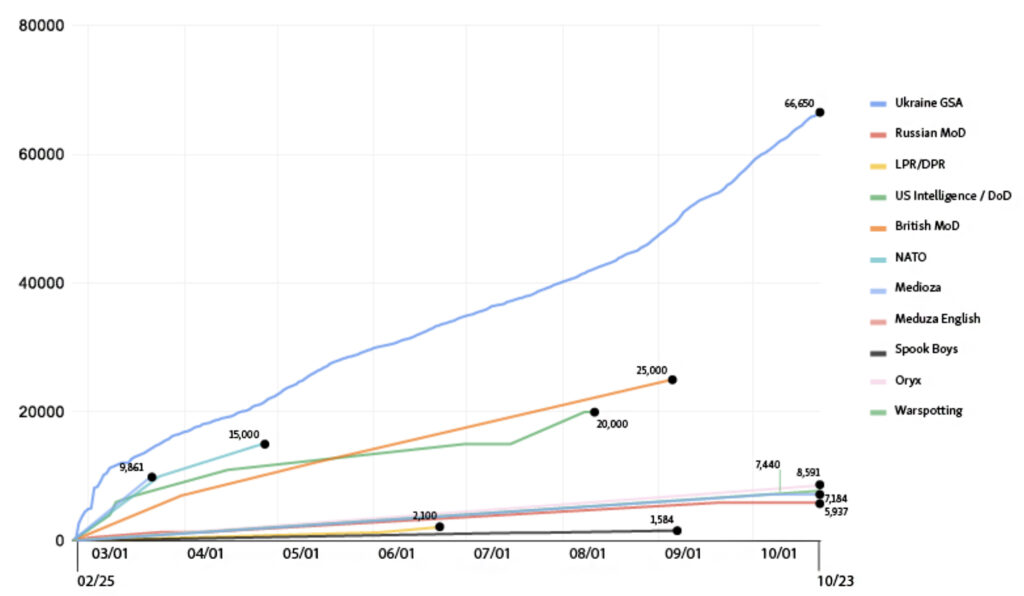

How are the human and material losses to be estimated? The Ukrainian, Russian, British and American defence ministries and intelligence agencies publish estimates of Russian losses. Ukraine, for example, publishes the number of Russian soldiers it claims to have killed each day, together with details of the missiles used by Russia and the materiel destroyed by Ukraine. For its part, Russia gives little information about the losses it suffers, despite the growing mobilization of troops that makes this ‘special operation’ feel increasingly real to its population. All these communications are to be seen in a context of war, where they act as instruments of disinformation. To preserve the morale of its population and its allies, each party to the conflict has an interest in downplaying its losses and overestimating those of its opponents. In the Ukrainian case, overestimating the rates of attrition of materiel may also represent an argument for arms shipments to them to be speeded up.

Beyond the official announcements, estimates are available based on fact-checked losses, using open access sources on social networks or local media. Where human casualties are concerned, the Mediazona site counts the number of deaths among Russian soldiers,1 drawing mainly on photographs of bodies published by their nearest and dearest or announcements of the dates of funerals. It has in this way visually confirmed at least 14,000 Russian soldiers killed since the beginning of the conflict, not counting the losses in the self-proclaimed republics of Luhansk and Donetsk.

On material losses, the Oryx site also publishes figures for those confirmed visually by photography or video for both the Russian and Ukrainian forces.2 These are divided up into destruction, damage and capture of equipment (tanks, vehicles, artillery etc.). Ballistic and cruise missiles, which are able to strike targets over a long distance are not included in these figures, nor is the consumption of artillery shells or rockets. This source provides, then, a useful indication of the intensity of the fighting, of the degradation of material systems, but not of the consumption of munitions, which is the main attritional factor affecting the stockpiles and industrial systems of Russia and the Western nations. On this question, we have then to refer to the intensity of fire reported in the media and the estimates of the belligerents’ pre-war stockpiles, which, given their strategic importance, are inevitably only approximations.

Cross-comparing these sources shows relatively similar trends with regard to rates of human and material attrition. For example, there is still a high level of consumption of shells, but this has been trending downwards for several weeks,3 whereas numbers of human losses seem to be rising as Russia has deployed its ‘meat grinder’ strategy in the Bakhmut region.4 By contrast, comparing the absolute figures cited in the various sources shows up major disparities. To take the example of Russian soldiers reported killed, Ukraine estimates 140,000 as of mid-February,5 the UK and the USA around 50,000,6 while Mediazona gives a figure of at least 14,000. Work based on open access sources provides minimum estimates. The Ukrainian figures are particularly high and the Russian figures low, so that UK and US estimates have come to be regarded as the source deemed most reliable. The figures they provide represent, by default, a mid-level estimate regarded as acceptable, even though they are not neutral actors.

Figure 1. Estimate of the Number of Russian Dead between 24 February and 22 October 2022 according to various sources

Source: Tweet OSINT EAST, 25 October 2022. URL: https://twitter.com/osint_east/status/1584725957902233600/photo/1. Accessed 21 February 2023.

However, estimating the number of soldiers killed is insufficient to establish an army’s total losses: the wounded and captured have to be added in and the Ukrainian authorities do not communicate figures for these. To arrive at numbers, analysts use a ratio of the number of soldiers killed to the number wounded. That ratio varies historically depending on the type of conflict, the sophistication of offensive and defensive equipment, and also the quality of the medical services in the field. For the USA in Afghanistan, that ratio was 1:10 in an asymmetric conflict with a low intensity of artillery exchanges and rapid airborne medical support available. By analogy with the Second World War and the Russian intervention in Afghanistan, a ratio of around 1:3 is generally applied by UK and US intelligence services in the Ukrainian conflict.7 The armed forces of the People’s Republic of Donetsk have documented their losses precisely, indicating a ratio of 1:4. This has not, however, settled the debate, with some estimating that medical advances and protective gear, together with the move to artillery warfare that is more likely to cause non-lethal injuries, ought to bring the ratio closer to 1:5. If this last figure were used, the losses deduced from the Ukrainian figures for Russian dead would not match up with the number of soldiers initially mobilized, which highlights the great uncertainty surrounding the data in this area.8

Lastly, let us remember that the rates of attrition for humans and equipment, together with their renewal through the logics of flows and stocks, remain subordinate to a variable that is difficult to quantify, yet crucial: the willpower of the belligerents. The fierce determination of the Ukrainians to defend their national sovereignty, symbolized by the personality of President Zelenskiy, has since the beginning of the conflict ensured that they have had greater resolve and higher morale than the Russian invaders. Contrary to the claims of Vladimir Putin, for the Russian combatants this special operation does not represent an existential issue for the nation. The attraction of money for the volunteer fighters, the promise of freedom for the convicts mobilized from prison—and also the compulsion of the more recent mobilization—seem to be less powerful forms of motivation than those offered to its soldiers by Ukraine. The Russian meat grinder strategy must, however, be analysed in a specific cultural context—that of a relationship to suffering and death that is different from Western societies and that harks back to the ‘Great Patriotic War’. With the mobilization of Russian society set to intensify, bringing inevitable tragedy to soldiers’ families, this war could become a more vital issue for Russia. The determining factor might then be whether the West can sustain its resolve to support Ukraine, as financial and material costs rise, the socio-economic context in Europe potentially deteriorates and the possibility of an escalation of the conflict continues to loom frighteningly.

1. ‘Russian Casualties in Ukraine. Mediazona Count, Updated’, Mediazona. URL: https://en.zona.media/article/2022/05/20/casualties_eng. Accessed 21 February 2023.

2. See ‘Attack On Europe: Documenting Russian Equipment Losses During The 2022 Russian Invasion Of Ukraine’, Oryx. URL: https://www.oryxspioenkop.com/2022/02/attack-on-europe-documenting-equipment.html. Accessed 21 February 2023.

3. Bertrand Natasha, Liebermann Oren and Marquardt Alex, ‘Russian Artillery Fire Down Nearly 75%, US Officials Say, in Latest Sign of Struggles for Moscow’, CNN, 10 January 2023. URL: https://edition.cnn.com/2023/01/10/politics/russian-artillery-fire-down-75-percent-ukraine/index.html. Accessed 21 February 2023.

4. Segura Cristian, ‘Battle for Bakhmut Turns into a “Meat Grinder” for Russian and Ukrainian Armies’, El País, 1 February 2023. URL: https://english.elpais.com/international/2023-02-01/battle-for-bakhmut-turns-into-a-meat-grinder-for-russian-and-ukrainian-armies.html. Accessed 21 February 2023.

5. Tweet by the Ukrainian Ministry of Defence, 16 February 2023. URL: https://twitter.com/DefenceU/status/1626112972895526913. Accessed 21 February 2023.

6. Tweet by the UK Ministry of Defence, 17 February 2023. URL: https://twitter.com/DefenceHQ/status/1626472945089486848?s=20. Accessed 21 February 2023.

7. Lawrence Christopher A., ‘Wounded-to-killed Ratios in Ukraine in 2022’, The Dupuy Institute, 6 June 2022. URL: http://www.dupuyinstitute.org/blog/2022/06/06/wounded-to-killed-ratios-in-ukraine-in-2022/#_ftn1. Accessed 21 February 2023.

8. ‘How Heavy Are Russian Casualties in Ukraine?’, The Economist, 24 July 2022. URL: https://www.economist.com/europe/2022/07/24/how-heavy-are-russian-casualties-in-ukraine. Accessed 21 February 2023.

Who are the Protagonists?

A Russia Weakened by War, but an Enhanced Mobilization of its Population: Towards a Flipping of the Balance of Forces in 2023?

The Russian economy has undeniably been greatly affected by the economic, trade, and financial sanctions, even if their short-term macroeconomic effects were less significant than initially anticipated. Whereas in April 2022 the International Monetary Fund (IMF) forecasted that Russian Gross Domestic Product (GDP) would shrink by 8% in 2022, its October forecast has fallen to just a 2% drop; they even anticipate, with a degree of optimism, that Russia will not see a recession in 2023.[14] But the real issue is the extent to which the Russian war effort is affected by these sanctions. For example, the restrictions imposed on its imports of technological components have affected its ability to produce high-precision missiles, stockpiles of which have seemed severely depleted since summer 2022. Russia appears, nonetheless, to have set up alternative supply chains, with the recycling of civilian technological products (household appliances, electronics and vehicle parts), imported from Turkey, China and countries in its central Asian neighbourhood.[15] More generally, the Russians have already begun to draw on lower quality Soviet-era equipment (T-62 tanks, reconditioned artillery shells) and on the sub-optimal use of anti-aircraft defence missiles (S-300 missiles) for offensive ground operations, which have turned out to lack precision.

Russia also enjoys direct Iranian military support, Iran’s drones having a cost-effectiveness ratio that is highly conducive to maintaining the current rate of bombing over time.[16] At the same time, the war of position that largely characterizes this conflict requires intensive use of artillery, which has, at times of peak intensity, been consuming shells at a rate similar to that seen by the USSR at the beginning of the Second World War (almost one million per month).[17] However, the Russian capacity to sustain the fight over time still remains uncertain. According to the American and Ukrainian intelligence services, the intensity of Russian artillery fire has fallen by at least two-thirds since late 2022. Material support from North Korea and Belarus attests to an exacerbation of these issues around missile stocks.

Where military matters are concerned, can Russia’s difficulties, which have been visible from the start of the conflict, be overcome? Some weak signals seem to indicate that they can, such as the prioritization of military imperatives over symbolic objectives (withdrawal from Kherson), better joint force coordination, and, most importantly, the gradual training of the new conscripts. This has admittedly been short and partially flawed, but it seems to have been better organized than was originally expected.[18] The ability to carry out large-scale offensive manoeuvres in the next few months does, however, remain highly uncertain, given the logistical, equipment and command constraints the Russian army has to cope with.

With regard to public opinion, the impact of sanctions on the population, and also the enhanced military mobilization contribute to bringing the war closer to home and hence making it more unpopular. Nevertheless, though there is no massive support for the elites, the predominant mood seems to be passive. On the other hand, private military contractors, such as the leader of the Wagner Group, Yevgeni Prigozhin, seem to be attempting to exploit the Russian army’s failures for their own political ends.[19] Despite the opaqueness of the Russian political situation, it does, however, seem possible to say that the structure of Vladimir Putin’s regime, organized around the siloviki clan,[20] is not under threat at the moment.

Moreover, Russian society is now increasingly involved, with an intensive use of propaganda appealing to the imagery of the ‘Great Patriotic War’. Military and security expenditure has doubled since the start of the conflict, while the requisition of civilian industries for military purposes has been authorized by decree.[21] This transition to a war economy could, among other things, speed up the dynamics of the replenishment of Russian weapons stocks (including artillery shells).

In this way, if Russia continues its hard-line logic without coming up against a significant Ukrainian counteroffensive before autumn 2023, the dynamics of the balance of forces between the two belligerents might turn around again—this time in Russia’s favour.

Ukraine on Western Life-support. How Sustainable is the War Effort to 2025?

In Ukraine, a general mobilization was decreed at the start of the conflict. The Ukrainian forces, trained by the American and British military and with experience of fighting in the Donbas since 2014, proved to be particularly effective. The number of Ukrainian soldiers lost is difficult to estimate (see section ‘How to Gauge Levels of Attrition…’ above), but they were of an order of magnitude comparable to that of the Russians in late 2022, Russia having almost 100,000 casualties at that point.[22] The employment of a ‘meat grinder’ strategy by Russia in the Bakhmut region, drawing on the new wave of mobilization, sharply accelerated the pace of Russian losses and, to a lesser extent, those of Ukraine.[23]

In terms of equipment, Ukraine is still on the wrong side of the balance of forces in terms of artillery (by a ratio of one to three).[24] But shipments of more than 300 modern NATO systems from spring 2022 onwards have produced a notable strategic shift, having significant effect and reducing rates of attrition. However, in the face of the strengthening of Russian forces, the maintenance of the Ukrainian war effort depends on the scale and adaptedness to need of the shipments of NATO weapons and their continued supply, on which it is dependent. The Russian military budget of 60 billion euros was ten times greater than Ukraine’s before the start of the conflict.[25] The 40 billion Western dollars, supplied to Kyiv in the form of loans and donations, go a long way to rebalancing the situation.

The contribution of European countries to this support, expressed as a proportion of their military budgets, is greater for the countries of Central and Eastern Europe, which have historically had a more acute sense of the Russian threat. But, in the absence of a reorientation of the industrial policy of European nations to a war economy, their low stockpiles of military equipment mean that the burden of this support falls very largely on the USA. Between February and November 2022, it provided assistance to Ukraine at a historic level of almost 23 billion US dollars.[26] That represents 60% of the total military support announced for Ukraine, European support coming more in financial and humanitarian form. The total support expenditure will also include that intended for rebuilding the country. Given the destruction of Ukrainian civil and energy infrastructure since October, the total bill could reach between 500 and 1,000 billion US dollars, depending on the intensity and duration of the conflict.[27]

Figure 2. Government Support announced for Ukraine by Type and Country (Between End of January 2022 and 15 January 2023) (in billions of euros)

Source: Kiel Institute for the World Economy, ‘Ukraine Support Tracker’ page, op. cit.

If the conflict were to reach a stalemate lasting several years, are these flows sustainable? An analysis by the Center for Strategic and International Studies (CSIS) shows that—as for the Russians—there will be greater shortages of artillery shells and missiles than of launch systems. Replenishing American stocks of HIMARS and multiple-launch rocket systems (MLRS) will take several years, though shipments of less modern systems may fill the gap. However, supplies of missiles adapted for use in these systems in Ukraine seem limited (one-third of the American stockpile would represent only a few months’ consumption).[28]

The scale of the limitations in terms of material and human resources to which Ukraine—and Russia—are subject remains highly uncertain. Given the estimates mentioned above, we may, however, assume that a stalemate in the conflict lasting several years would necessitate a decreased combat intensity, if it is to be sustainable. This prospect of a ‘forever war’ might bring continuing Western support into question, with pressure coming from public opinion and political parties. In January 2023 almost a quarter of all American voters—and 40% of Republicans—took the view that too much support was going to Ukraine (as against 12% and 17% in May 2022).[29] It is not, therefore, impossible that Washington’s support may be called into question by 2024.

Figure 3. Heavy Weapons: Comparison of estimated NATO stockpiles and weapons publicly announced as shipped to Ukraine, by category of weapon (between end January 2022 and 15 January 2023)

N.B.: Data from the International Institute for Strategic Studies (IISS), The Military Balance, counting only weapons that are combat-ready.

Source: Trebesch Christoph et alii, op. cit.

The USA as the Major Winner in the Conflict: Towards a Consolidation of American Power on the International Stage and in Europe

Of the participants in the conflict, the USA seems to be the major winner, to the detriment of Europe, so far as the economic and trade dimensions are concerned (cf. key message 12). Though US deterrence efforts failed to prevent the conflict, the USA would seem to have subsequently increased its credibility through its support for its allies—via sanctions, military aid and the power of its intelligence apparatus etc. Furthermore, the nuclear threshold has still not been crossed by Vladimir Putin, the American threat of a robust conventional response probably playing a part in deterring him. Since the Cold War, NATO has never been as credible and well-supported as it is now, even if the anti-Russian front has remained limited to the USA’s historical allies on the world stage. At the same time, China has probably scaled back its strategic estimation of the chances of conquering Taiwan at minimal cost, at least in the short term.

From the commercial standpoint, the Americans have greatly increased their gas exports to Europe. Their national industry has grown more competitive in a context of energy inflation in Europe and Asia, a phenomenon exacerbated by a policy of massive national subsidies through the Inflation Reduction Act.

At the same time, France’s calls for EU strategic military autonomy from NATO have come to nothing, with significant recourse being had to orders of materiel from America and South Korea (on the part of Germany and Poland). This raises the question of the EU’s strategic credibility, at a point when the USA might pivot back to a new isolationist Republican president in 2024 or shift to a more exclusive focus on their Chinese rival at that juncture

Turkey, a Regional Power Central to the International Issues of the next few Years

Turkey occupies a strategic geographical position at the crossroads of Europe, Africa and Asia. It finds itself, for example, at the heart of the reorganization of gas networks towards Europe and of the issues around control of the Black Sea straits. For several years now, the country has played an ambivalent role, walking a tightrope between the two parties to the conflict. As a member of NATO, it did not recognize Russia’s annexation of the Ukrainian regions and defends maintaining Ukraine’s territorial integrity. But, while selling drones to Ukraine, it is also trying to advance its national interests through trading in energy and food with Russia or vetoing Sweden and Finland’s membership of NATO. Turkey is also a major alternative trading platform for Russia,[30] in part enabling it to evade sanctions (on electronic components, energy etc.).[31] Moreover, the country continues to be involved in what will be the geopolitical ‘hotspots’ of the next few years: military operations in the north of Syria, tensions in the Eastern Mediterranean (with Cyprus and Greece) where there are gas reserves that could potentially be exploited to provide a significant proportion of European supplies in the 2030s.[32]

This is a paradoxical situation, since Turkey is perhaps the most appropriate mediator to resolve the conflict, making it a country of fundamental strategic importance within NATO. But is there not a risk, by granting too many concessions, of reproducing past errors and underestimating the dangers of a new energy dependence, as previously with Russia? If President Erdogan stays in power, in a context of high inflation, the hypothesis that the period to 2030 will see Turkey pursuing an expansionist regional policy no longer seems so improbable.

Nevertheless, the February 2023 earthquakes in Turkey and Syria will potentially have massive regional impacts that could lead to a weakening of Turkey’s status as a regional power in the medium term. Given the inflow of vulnerable people, there will be considerable tensions in the coming months, against a background of economic, social and humanitarian crisis. Whether the current Turkish regime will remain in power or whether it may possibly become more hard-line is now an open question. Depending on how the country plays things geopolitically in the coming months and years and the scale of Western aid, the region could be destabilized.

China and Russia: Interests strongly Converging, but as yet no Overt Military Alliance

The world of blocs described in our scenario no. 2 has not, for the moment, found expression in China aligning itself with Russia as overtly as Iran or North Korea. The increased tensions those countries have experienced with their—Israeli and South Korean—neighbours attest to a certain overlapping of the fronts of different conflicts, in which the polarization of alliances and perceived opportunities for ‘power grabs’ fuel the rise in tension. For example, faced with the threat of Iran obtaining nuclear weapons, Israel could leverage NATO opposition to drone shipments to Russia from Teheran to mobilize a coalition against the Shi’ite regime.[33]

Though it does not support the Russian invasion of Ukraine and is not, for the moment, supplying arms, China is nonetheless part of a common ideological front with Moscow against the USA. The two countries made a joint declaration back in February 2022, defining together a ‘new era’ in international relations and ‘sustainable global development’. Above and beyond the individual affinities between leaders Vladimir Putin and Xi Jinping, Beijing has also boosted its trade with its neighbour against a backdrop of Western sanctions. That trade increased by nearly one third in 2022 by comparison with 2021.[34] In particular, imports of Chinese products are slightly up (by 13%), whereas most of Russia’s trading partners have greatly reduced their exports and investments as a function of Western sanctions.[35]

Some trade flows are, however, still limited by infrastructure-related inertia. The reorientation of gas deliveries to China will not exceed 50 cubic gigametres by 2025, which is just one third of the volume exported to the EU before the conflict.[36] Supply through the Power of Siberia II pipeline is not, in fact, expected to begin until 2030 (an additional capacity of 50 cubic gigametres). The pivoting of Russian energy flows towards Asia will, however, enable Beijing to reinforce its energy security cost-effectively.

The difficulties encountered by the Russian army on the ground have probably played a part in damping down China’s warlike inclinations toward Taiwan. But the conflict is also providing lessons for China and helps to drain American military reserves. In the medium term, might we see the emergence of a military alliance with Russia that forces the USA to choose between two fronts, to the detriment of Europe? Combined with the Russian rapprochement with the Iranian and North Korean regimes, are we witnessing the formation of two blocs, the one authoritarian, the other democratic, around which future global conflicts might be structured?

What are the Broader Geo-economic and Geopolitical Consequences?

Greater Trends toward National Autonomy, but Continued Interdependence: De-globalization still a Fantasy

Whereas the percentage of international trade in global GDP rose from 25% in the 1970s to almost 60% in the early 2000s, a plateau appears to have been reached since the 2008 financial crisis. Might that slowdown herald a new phase of de-globalization? Elvire Fabry, a senior researcher at the Institut Jacques Delors and scientific adviser to Futuribles International, reminds us that this plateauing is linked to a short-run effect of the prices of extractive and fuel products (one quarter of the volumes traded) falling over the decade. Data and service flows continue to grow and the emerging countries continue to look to their insertion into globalization’s value chains to bring them development. What we are seeing, then, is more of a reorganization of globalization that might ‘equally well lead to the coexistence of rival blocs or to an escalation in retaliatory measures and a fragmentation of global value chains’.[37]

The pandemic and the war in Ukraine have highlighted the vulnerabilities of states to external shocks in a globalized economy with high levels of interdependence. Looking to 2025, the development of Chinese economic activity will continue to affect international value chains, with prospects of a lasting slowdown if the epidemiological or geopolitical situation deteriorates. Improving the resilience of supply chains, which were historically an issue for businesses, has today become a concern of states.

Within the EU, the on-shoring of strategic value chains (healthcare products, batteries, critical metals etc.) is a political objective that has come to be increasingly advocated since the pandemic and the formulation of the concept of ‘strategic autonomy’. For example, in a report published in February 2022 that forms part of the European industrial strategy, the European Commission identified 137 products on which Europe has significant strategic dependence, half of these being dependent on China.[38] These products consist mainly of raw materials and of processed products in the chemical, health, and digital and ecological transition technologies sectors. Among the dependencies, 34 are said to be particularly critical given the limited scope for diversification and substitutability. For the moment, however, there has not been any significant on-shoring of European companies from China. According to a European Bank of Reconstruction and Development (EBRD) survey, in the spring of 2022 European companies had mainly chosen to increase their stocks of inputs (55%) and diversify their sources of supply (49%).[39]

Implementing a common EU strategy of uncoupling from China looks complex, since the various countries have differential levels of commercial dependence, as was highlighted by the visit of Chancellor Olaf Scholz to Beijing on 4 November 2022, a visit aimed at fostering economic relations between the two countries (China being German’s leading supplier and its second largest export market).[40] Most importantly, the reconfiguration of production chains continues to be constrained by the availability of skilled labour, the location of raw materials and the social acceptability of their domestic exploitation. In a context of rising energy costs, the reindustrialization of Europe seems highly uncertain. The diversification of supply chains along the lines of the bilateral agreements signed by the EU for importing energy-transition materials (with Chile, Kazakhstan and Namibia etc.[41]) will also raise the issue of what political logic there may be to those agreements with potentially undemocratic partners. In this context, we might see an increase in the number of trade agreements at a regional level or among friendly countries (the so-called ‘friend-shoring’ of value chains).

At the global level, competition for access to strategic raw materials in a tense geopolitical context seems set to increase greatly and could lead to conflicts, direct or indirect, between powers. Some African countries are directly affected.

Emergence of a China-US Decoupling over Strategic Sectors

Sino-American trade decoupling is set to intensify in a context of growing rivalry. It has up to this point been sectoral: American imports of ordinary consumer goods, which are not subject to the tariffs that increased by 25% during the Trump presidency, have risen by 50% since 2019.[42] The Biden presidency has stressed the primacy accorded to national security in trade policy, as well as the maintenance of the greatest possible technological lead over China. In October 2022 the USA adopted a strategy in line with the EAR (Export Administration Regulations)[43] that widens restrictions on the export of strategic technological components to China, so that they apply extraterritorially and to products beyond the military sector (chips, advanced semi-conductors for use in artificial intelligence, supercomputers and biotechnologies).[44] At the same time, the dependence on Chinese energy transition technologies will be reduced as a result of the Inflation Reduction Act, a programme of massive investment in ecological transition. As regards China, its strategy of upgrading its production at earlier stages in value chains has not yet enabled it to reduce external dependence on high technology. Xi Jinping’s time in office has, however, seen greater importance accorded to issues of national security and autonomy, rather than purely quantitative economic growth through international trade.[45]

There continues to be great uncertainty over the Americans’ ability to bring international partners on board in this hardening of trade policy towards Beijing. Above and beyond the emerging powers, which pursue a pragmatic trade policy (Turkey, India and OPEC), China’s neighbouring countries are, in fact, strongly commercially dependent on it, as are some states in the Global South via the mechanism of debt. An intense battle over standards can also be foreseen at the international level as part of Chinese-American rivalry, relating to the spread of new technological innovations (6G, digital currencies, hydrogen and synthetic fuels etc.). The extent of European alignment with the American strategy remains uncertain (cf. key message 12).

Might we see a high-intensity economic war between China and the USA emerge in the coming years? To what extent will these two players be able to curb the escalation of retaliatory trade measures that is currently underway and how far might that escalation go?

Lasting Tensions in the Energy Markets: Towards a ‘De-continentalization’ of Europe’s Oil and Gas Supply?

Before the conflict, approximately 40% of EU primary energy consumption in the form of gas was dependent on Russian imports. The figure for coal was 30% and for crude and refined oil taken together, 25%. The short-term shock experienced by the gas markets, particularly as a result of the sanctions policies implemented by Europe and Russia, is exacerbating the tensions over energy security that were already present on account of the decline of controllable production capacities in Europe (maintenance work on nuclear installations, the closure of fossil-fuel-fired power stations). At the same time, the very structure of the European electricity market is intensifying the price-rise contagion from gas to electricity.[46] Visions for European reform of that market will face strong structural oppositions between national energy policies, particularly over the funding mechanisms for renewable, nuclear and fossil-fuel production capacity.[47]

The rise in prices enabled Russia to achieve historic energy revenues in 2022, but the much larger foreseeable fall in volumes exported to Europe will undeniably affect Moscow’s budget in 2023. The shifting of flows of Russian gas towards China will only be able to compensate for this deficit at the margins, since those flows are limited by the amount of time it will take to develop new pipelines.

A. Historical Volumes

Figure 4. Russian Oil and Gas Exports (in billions of US dollars)

B. Projections 2022-2024 by scenario

Base case scenario: cap on Russian crude oil at 55$/barrel. Bear case scenario: 75$/barrel. Bull case scenario: 35$/barrel + sanctions against LNG (liquefied natural gas).

N.B.: the G7 set a cap of 60$/barrel in December 2022.

Source: The International Working Group on Russian Sanctions, ‘Implementation of the Oil Price Cap’, Working Group Paper 10, 28 November 2022. URL: https://drive.google.com/file/d/1jIQDNfIPTENaW6gGv-ZiEEem7N94UF1A/view. Accessed 21 February 2023.

Where oil is concerned, by contrast, the war has had only a moderate effect on prices as yet, largely on account of America drawing on its strategic oil reserves. Russian hydrocarbons have already begun to flow away from the European and into the Asian market. Indian imports of Russian crude oil have increased dramatically since the start of the conflict. Moscow has become the main supplier, ahead of Saudi Arabia and Iraq, and now provides more than 20% of India’s oil imports, as opposed to less than 1% before the conflict.[48] With Indian fuel standards being compatible with the European, this has played an indirect role in the supply of diesel to the EU, Indian exports to Europe being up by one third.[49] Russia has also been the leading oil supplier to China since May 2022, exports of Russian crude having increased by a half in 2022 over the 2021 figure.[50]

The establishment in November 2022 of the EU embargo on crude oil from Russia and that of February 2023 on its petroleum products is aimed at limiting volumes exported. At the same time, the adoption by the G7 of a cap on oil prices (60$/barrel) aims to reduce Russian revenues, even if that effect will be moderate, given the discounts already offered to Asian buyers by Moscow. While oil prices are relatively uniform internationally, unlike prices in the regional gas markets, the sanctions affect the price of the Russian Urals barrel, which currently stands at around a half of other international reference prices, such as North Sea Brent (see figure 5). Uncertainties remain as to how far Russia is potentially evading these sanctions. We are already seeing the increasing mobilization of a ‘ghost fleet’ of ships that played a part in evading the oil embargoes on Iran and Venezuela substituting for the fleets of Western companies, which are applying the sanctions.[51]

Figure 5. Reference Prices of North European (Brent) and Russian (Urals) Crude Oil 2022-2023 (in US dollars per barrel)

Source: Mills Robin and Mehdi Ahmed, ‘The EU Ban on Russian Oil: Crude Implications for the Middle East’, Center on Global Energy Policy at Columbia, February 2023. URL: https://www.energypolicy.columbia.edu/wp-content/uploads/2023/02/EU-ban-on-Russian-oil-Commentary_CGEP_021023-6.pdf. Accessed 21 February 2023.

These Western sanctions thus aim to achieve a precarious balance between lowering Russian energy revenues and maintaining global supply by displacing Russian exports to other destinations. However, Europe might experience increased tensions over the price of diesel in 2023 if there is insufficient growth in imports of refined products from India and the Middle East. Where gas is concerned, the main adjustment variable for European supply will be demand, both domestic and international. As of late 2022, the EU received only 15% of the Russian gas it imported by pipeline before the conflict, forcing it to seek supplies from the—very high-cost—LNG market.[52] Since there is little chance of the available global volume increasing by 2025, this will involve competition with the Asian countries. The poorest nations (Bangladesh, Pakistan etc.) will continue to experience growing inflation and repeated shortages. By 2025, the evolution of Chinese demand will be the crucial factor for the security of European supply, against the backdrop of an uncertain economic and health situation.

Nicolas Mazzucchi, Research Director at the French Navy’s Centre for Strategic Studies and a Futuribles International scientific adviser stresses the major geopolitical implications of this ‘de-continentalization’ of the European energy supply. The gas and oil pipelines from Russia and Central Asia will no longer be the main strategic paths for the Old Continent’s energy security. In 2022 we were already seeing a rise in LNG imports and petroleum products from the USA, the Middle East and India. The redirection of international flows in the years to 2025 and, most importantly, in the longer term, the development of new export projects (Qatar, Eastern Mediterranean) will increase the strategic importance of the maritime supply routes in the Mediterranean and the Indo-Pacific.

It is highly probable, then, that gas and oil prices will remain high on the wholesale market in the coming years. In an unstable geopolitical and economic context, there is likely to be greater price volatility. Up to now, households and companies have partly been protected from this inflation by state action, though in an unequal way between countries and categories of consumer. But, given the unsustainability of this public spending, the protection offered by ‘energy price shields’ could be cut back in the years to 2025, putting pressure on the budgets of vulnerable households and companies.

The frequency and extent of shortages in Europe will depend on the level of demand, which has so far reduced, mainly thanks to the reduction in economic activity, particularly industrial activity,[53] but also to the self-restraint of communities and households. Eurostat’s industrial production index shows a stability in the volumes of manufacturing production in Europe between November 2021 and 2022. On the other hand, the energy-intensive sectors are particularly badly affected, such as aluminium (down by 20 %), chemicals, steel and ferro-alloys (down by 15 %), cement (down by 10%) and paper-making (down by 7 %). The European fertilizer industry claims to have had to reduce its production capacities by 70% in the peak price periods of summer 2022, while the German chemicals industry giant BASF announced it was planning a long-term reduction of its activity on the Old Continent.[54] In another example, the world’s second largest steel producer, Arcelor Mittal, decided in September 2022 to halt production at three of the 16 blast furnaces it operates in Europe.[55]

Fears of a Major Global Food Crisis not yet Realized, but Risks Remain

According to the United Nations Food and Agriculture Organization (FAO), Ukraine and Russia accounted for around a quarter of global grain exports before the conflict, Ukraine for half of sunflower oil exports, and Russia for between 15 and 20% of nitrogen-potassium-phosphorous fertilizers. The countries dependent on these imports are those most vulnerable to a price rise: approximately 30 countries, 12 of them in Africa, get more than half of their grain imports from Ukraine and/or Russia. However, fears of a global food crisis related to the conflict have not yet been realized. Agricultural commodity prices did, admittedly, increase greatly in the months following the start of the war, on account of the uncertainties over Ukrainian production and its exportation—uncertainties exacerbated by acts of speculation. But the agreement in late summer on the export of cereals calmed the situation: half of Ukrainian grain inventories are thought to have benefited.[56] This agreement does, however, remain fragile, though Russia seems to have realized the difficulty of pursuing ‘hunger diplomacy’ to undermine the West’s credibility with its partners in the global South.

Certain factors could, however, give rise to increasing tensions in the coming months, while climate change is, at the same time, having its effects on the productivity of agricultural land. These are:

— Inflation in mineral nitrogen fertilizers, on account of sustained high gas prices, even though these are currently back at their late 2021 levels (in developed economies, fertilizers represent, on average, almost a third of the costs of the harvest[57]).

— Further intensification of the export restrictions imposed by some countries, particularly in Asia (e.g. grain, sugar, rice in India;[58] fertilizers in China[59]). In the first ten months of 2022, 166 export restriction measures on foodstuffs and fertilizers were introduced worldwide, two thirds of them by G20 countries.[60]

— Expansion of the war zone in Ukraine. In August 2022, half of agricultural land and cereal production areas remained outside occupied or disputed territory.[61] Though the fronts have not shifted much since that point, their potential extension to the Black Sea coast or, indeed, the use of chemical weapons, could appreciably reduce Ukrainian cereal exports.

The countries that are most dependent on imports of agricultural inputs and products will be the worst affected by this price rise and by protectionist policies. The significant appreciation of the US dollar in 2022 made for additional pressure on import costs.

Economic and Political Dissensions within the EU: The Future of European Equilibrium Unresolved

The rise in energy and food prices is exacerbating the European inflation that occurred in the context of expansionary monetary policies and the post-Covid resumption of international trade. At the time of writing these key messages, inflation seems to have reached a peak in Europe, with the feared wage-price spiral not materializing. Uncertainty remains, however, around how inflation will develop, as the rise in energy and food prices has not yet worked through to all companies and households.[62] This situation inevitably gives rise to political and economic dilemmas within EU member states (interest rate rises v. slowdown of growth and unemployment; maintenance of public expenditure v. increased national debt, etc.).

In this context of great pressure on public expenditure, the European institutions actually find themselves faced with the need to adopt unconventional policies, as they were during the pandemic. Against a backdrop of trade war, a relaxation of the rules on state aid and common European investments is envisaged, as laid down in the European strategic Industrial Green Deal plan that was published in early February 2023. It is the same with the jettisoning of rigid budgetary and monetary targets (budget deficit not to exceed 3% of GDP and debt to remain below 60% of GDP) in favour of targets more suited to the profiles of the member states, but with increased oversight that may be accompanied by prescriptions for structural economic and financial reforms. Moreover, the aid associated with stimulus packages is conditional on investment conforming to ecological and digital transition targets, and also on reforms of the justice and political systems (cf. Poland[63]).

Are we moving, in this way, towards an ‘IMF-ization’ of the European Commission? And how sustainable is that, particularly if member states continue to diverge in their trajectories? Is the Eurozone in danger?

Moreover, we are seeing a political and military re-balancing within the EU as a direct consequence of the conflict. The countries of Central and Eastern Europe advocate a hard line against Russia, viewing Paris and Berlin as insufficiently committed to supporting them. In the face of the threat, Poland is rearming massively and could become the future leading military power in the EU, alongside the nuclear power, France.[64]

If, for the moment, the existence of the Russian enemy makes it possible to show a united political front and assert shared values, fundamental disagreements persist between member states over cultural and democratic models. The question of Ukraine joining the EU and the extension of the single market will exacerbate these divergences. They are already showing up in what are at times diametrically opposed positions, with some, admittedly in a minority, calling for the Russian Federation to be dismantled to ensure lasting peace, and others, such as the Pope, still pushing for negotiations with the Russians and keeping up diplomatic connections with them, despite the difficulty of expressing that view publicly. Austria, for example, refuses, in the name of its constitutional neutrality, to provide weapons for Ukraine and even to give tank-fighting training to its soldiers.[65] This being the case, though European rearmament seems necessary in view of war making a reappearance on the continent, might it not also lead, in the longer term, to a return of intra-European conflicts?

There is also a non-negligible risk of heavy-weapons trafficking within Europe and hence of a marked resurgence of terrorist movements or criminal networks. Russia could seek to stoke tensions in the Balkans, while at the same time continuing its information strategy of supporting right-wing populist movements. As for the humanitarian impact of the earthquakes of 6 February 2023, with several tens of millions of people affected, four million people in Turkey left vulnerable and potentially in a state of humanitarian distress, this is already substantial and could have effects on Europe. The figures for vulnerable people are similar for Syria, according to a statement by Sivanka Dhanapala, the representative of the UN High Commission for Refugees (UNHCR), at a press conference in Damascus.[66]

Above and beyond its economic equilibrium, then, the EU’s political and security equilibrium is also left unresolved.

Part 2. Updating of the Scenarios

Scenario 1. Stalemate and Instabilities

Reminder of the Key Points envisaged in July 2022

This scenario envisaged that the military conflict in Ukraine would remain frozen until 2025 and consequently front-line zones would stabilize at the borders of the Donbas and along the corridor towards Transnistria, with Odesa remaining in the hands of the Ukrainians. However, as part of that course of events, the conflict would spill over into the cyber-world with repeated attacks on strategic infrastructures or sensitive sites and disinformation being carried out, including in other countries, with destabilization as its aim. In this context, the balance of forces is precarious and there is a high degree of unpredictability, despite the absence of an escalation in clashes on the ground. Geopolitically, in terms of alliances, the Ukrainians still enjoy Western support for this course, without that support being sufficient to tip the balance of forces in their direction. As far as Russia is concerned, the assumption was that it could maintain its war effort thanks to its sizeable trading revenues in spite of sanctions, but without support from substantial allies like China, which would remain neutral.

Update

• Militarily, at the time of writing, this first scenario seems to square with the succession of phases of conflict seen since February 2022: stalemate on the ground and a war of position, convulsive upsurges of violence, hybridization into the cyber field and the manipulation of instability by Russia through its disinformation channels, including in other countries… However, the fighting has not decreased in intensity. It has, rather, remained more or less constant, as a result of the two parties readjusting their war efforts. The Ukrainian forces have actually demonstrated great resilience, thanks among other things to the continuance of Western support (cf. key message 4). At the same time, Russia has also succeeded, by the greater mobilization of its population, in maintaining the pressure on the Ukrainian army (cf. key message 3).

→ By 2025, if events continue along this trajectory, the Russians might manage to freeze the fronts as initially envisaged, without necessarily achieving any further conquests. This hypothesis does, however, assume an increasing mobilization of the Russian population in the wake of the call-up carried out in autumn 2022 and industry being shifted onto a war footing. It also assumes a state of apathy in public opinion, as has been seen so far, in a situation where the country’s economy may be declining over the coming years, partly as a consequence of declining energy revenues and in the absence, largely for logistical reasons, of a total switchover of trade flows towards Asia by 2025.

• Geopolitically, China, though cautious, is not as neutral in the conflict as was initially foreseen (cf. key message 7). It is clear today that China is supporting Russia and opposing the USA.

→ Though China may have temporarily put on hold its thoughts of a military conquest of Taiwan in light of the Russians’ failure to make headway in Ukraine, the state of latent conflict with the USA might still deteriorate in the coming years, playing a role in the general instability that characterizes this scenario.

• Lastly, geo-economically, despite there being no ceasefire, the international initiative to keep exports flowing, though precarious, has made it possible, among other variables, to tamp down tensions in agricultural markets.

→ Other factors are, however, at play in the determination of market prices (appreciation of the US dollar, climate, fertilizer costs, speculation etc.) and pose questions over possible rises between now and 2025.

Overall, then, the logic of the conflict as laid out in this scenario in 2022, still applies in early 2023: the situation is characterized by an uneasy balance of military forces and political/economic alliances. And also by the regular occurrence of incidents with strong political and media repercussions, making for fears of an escalation of the conflict.

→ This scenario may, therefore, evolve at any moment towards one of the other scenarios described below.

Scenario 2. High Intensity Conflict in Ukraine. Towards a World of Blocs

Reminder of key points envisaged in July 2022

This scenario envisaged a geostrategic polarization of the conflict, finding embodiment on the ground and in international relations. While the Western bloc continues to support the Ukrainian war effort, China now stands unambiguously with Russia. This clear-cut opposition has much to do with an increase in the intensity of the fighting, still physically contained within Ukraine, but spilling over very widely into the cyber domain. Globally, the blocs are not yet perfectly cohesive by 2025, with major countries remaining non-aligned (India, Turkey etc.), but their existence can be seen in the progressive reorientation of energy flows, trade in commodities and humanitarian aid between ‘friendly’ countries.

Update

• Militarily, this scenario seems less in line with the situation as of early 2023 than Scenario 1, despite the deep strikes on the cities of Western Ukraine. The risk of overspill does, however, remain constant, though more as a result of international geopolitical tensions. For example, many dormant conflicts have been stirred back into life in recent months (Azerbaijan/Armenia, Kyrgyzstan/ Tajikistan, the Turkish incursion into northern Syria), while there is some danger of other fronts appearing (tensions in Transnistria, between Israel and Iran, China and Taiwan, and in Korea). NATO has speeded up its arms shipments to Ukraine, including now categories of equipment that it initially opposed sending (long-distance missiles, tanks etc.). To keep up its war effort, Russia has shown resilience through high levels of mobilization of its population against Western sanctions and in response to the rates of material and human attrition it has suffered. If the escalation in cyber-conflict has been more limited than was forecast in 2022, particularly with regard to the Russians’ limited capabilities, there has been an extension of information warfare, as for example in Mali and Burkina Faso.

→ Looking forward to 2025, the effects of the Russian mobilization are as yet uncertain, and the still very widespread denial of the impracticability of maximalist war aims may yet fade. If Russia is, in fact, unable to maintain or overturn the balance of forces by conventional warfare, it might consider an escalation in a hybrid format. Such a development could tip this scenario over into the other scenarios described below. Belarus might also become directly involved in the conflict.

• Geo-economically and geopolitically, at the time of writing this scenario appears to correspond to the current world situation. Though new blocs, in the sense of political and military alliances, do not seem to be forming, there are alignments between countries around anti-Western values and a shared interest in challenging American hegemony. Iran and North Korea have, for example, directly supported Russia with military hardware. Those states have also intensified their break with the international order in recent months, as witness North Korea’s ballistic missile tests, the stalled discussions over the nuclear deal, or Iran’s violent repression of social protests. For its part, China has remained cautious in its support, but has strengthened its trading links with Russia and is participating in sanction-busting. The hypothesis that China may directly support Russia by sending arms shipments is not to be ruled out, as the American Secretary of State Anthony Blinken has pointed out.[67] This could lead to a new escalation of tensions in Chinese-American relations, with the prospect of massive trade sanctions.

Conversely, Europe, North America and, more broadly, the member states of NATO are standing up to the authoritarian regimes, in this instance by way of more overt, formalized alliances. The impact of this geostrategic polarization on the reconfiguration of trade flows is already visible today, though mainly in the form of protectionist policies on strategic technological components rather than changes in energy and food flows. Despite the great tensions involved and Russian inclinations to pursue ‘hunger diplomacy’, an agreement on the Black Sea was signed this summer to allow the exporting of cereals, Russia having little to gain among the countries of the global South from putting further pressure on agricultural markets.

The opportunistic attitude of the ‘non-aligned’ countries initially envisaged in this scenario is manifesting itself only tentatively, the Organization of Petroleum Exporting Countries (OPEC+) having pulled off a diplomatic coup by symbolically announcing an intention to reduce production, despite a visit to Saudi Arabia by Joe Biden. Turkey, for its part, seems to have decided to carry on playing a role of opportunistic mediator and intermediary in the conflict. The natural catastrophe it has experienced recently could, however, produce a rethink on this (cf. key message 6)

Lastly, the pro-active use of humanitarian aid, presented in this scenario in July 2022 as a way of exerting soft power, appears today to have been an overestimation, in a context of economic crisis in which the financial scope for manoeuvre will be much reduced.

→ In the years to 2025, this polarization could intensify, with effects on the access to raw materials. Russia has lost its place as number one supplier of hydrocarbons to Europe, which has increased its dependence on American imports where gas is concerned. Nevertheless, the hypothesis of a clearly delineated bloc of ‘pariah’ states trading energy and food among themselves, mentioned in this scenario in July 2022, seems today too much of a caricature. Beijing actually seems keen to diversify its sources of supply, as is attested by the many long-term LNG contracts struck with the USA before the crisis, and its strategy towards Russia of taking advantage of discounted gas. Though technical constraints on infrastructure rule out a complete flipping of Russia’s energy flows in the direction of China within the next two years, China could emerge from the Ukraine war as the biggest winner in the medium term, having both reduced Russia to a vassal state and achieved great autonomy from the Western bloc. In the case of Iran, as of Venezuela, a return to pre-embargo energy revenues by 2025 thanks to the war seems highly unlikely today, on account of the excessive inertia in such systems and the costs of oil extraction. Moreover, it does not seem to be in Venezuela’s interest to join such a bloc of pariah states, given the current weak signals regarding the gradual reopening of the Venezuelan oil market and the diplomatic initiatives undertaken by Western nations (e.g. the meeting between Presidents Macron and Maduro at the COP27 conference on climate change at Sharm el-Sheikhin late 2022).

→ The reconfiguration of international relations seen today and described in this scenario is set to constitute the backdrop for the coming years, whatever the outcome of the conflict. But it will most certainly follow highly pragmatic logics that will perhaps play more of a role than the ideological principles that states often advance. This will contribute to clouding the geopolitical landscape in the years to 2025, to creating hybrid and ambiguous alliances, and to maintaining a certain form of trade globalization that runs counter to the notions of de-globalization widely touted since the Covid-19 crisis (cf. key message 8).

Scenario 3. Fears, National Self-Interest and Territorial Expansion of the Conflict

Key Points envisaged in July 2022

This scenario described a gradual withdrawal of the Western powers from the Ukrainian conflict, justified by an upsurge in a range of internal problems, both economic and social, and by American and European opinion turning against a continuation of the war for fear of escalation. NATO military assistance to Ukraine runs out of steam and the military balance eventually tips towards Russia. In this situation, Russia extends its occupation to the Eastern and Southern territories of Ukraine, without controlling them completely, and cuts off access to the Black Sea. In such a context, the Russians might issue more and more aggressive declarations against Poland, the Baltic States and Moldavia. This situation plays into a state of heightened tensions within the EU, which might then see intensifying conflict between member states.

Update

• Militarily, the logic of escalation seen since September is consonant with the conditions for this scenario. Russia has indeed undertaken a massive mobilization of its population since July 2022 and has partially repatriated its troops and militias that were in Syria and Africa. Though Ukrainian resistance has been more significant than was forecasted, it could still run out of steam. At the same time, although cyber-attacks have so far been limited, they might intensify in the coming months if Russia receives support in the form of foreign human resources (North Korea, China etc.). Furthermore, the nuclear threat remains at the heart of Putin’s rhetoric in an attempt to influence the outcome of the conflict.

→ Looking toward 2025, this scenario is still a plausible one if the Russian mobilization were to prove a strategic success, surmounting the difficulties over training, coordination and logistics that have been visible from the very start of the conflict. This would presuppose the qualitative success of that mobilization, above and beyond mere quantitative impact. A new wave of mobilization might also play into this scenario. Fear of escalation and socio-economic tensions represent important factors affecting a potential gradual disengagement of Western efforts. The Russians might also opt to extend the war to bordering countries, even though they do not currently seem to have the means to do so.

• Geopolitically, Russia’s ability to exert pressure over energy is now weaker than it was, there now being little room for manoeuvre when it comes to reducing gas supplies. Moreover, the destruction of the Nord Stream pipeline makes it difficult to resume gas flows, particularly as the other main gas pipeline (Yamal-Europe) runs through Poland, one of the countries most hostile to Russia. For the moment, impatience with inflation on the part of European populations remains less crucial as a factor in the development of the conflict than was initially expected. This is partly down to a relatively mild winter in 2022-2023, but also to the great resilience of the European internal market and the schemes rolled out nationally by member states to support companies and individuals. At the same time, China and India have already shown opportunism in the markets, as this scenario predicted. As for the USA, though the mid-term elections did not result in great success for the Republicans of a kind that could undermine support for the war, the 2024 presidential elections could still bring to power an isolationist candidate or one focused on China.

→ Looking to 2025, the very probable continuation of high prices in energy markets and the persistent risk of gas or electricity shortages in winter 2023-2024 might, however, lead to a wider questioning of support for the war, particularly if financial assistance to Ukraine is set against the needs of the European and American populations. The effect of the capping of oil prices by the G7 and the embargo on oil implemented by the EU are influential factors to pay attention to. Russia may, in fact, consider destroying other European pipelines towards Africa or Norway, at the risk of dramatically inflaming the conflict. This tense situation might then fuel conflict between member states over issues of economic and energy solidarity, as can already been seen today in the debates over the reform of the electricity market or the state aid mechanism. In an unstable context, the risk of the European Union fragmenting remains high.